Introduction

Republic

India Coinage is known for its "commemorative coins", and by saying

that I mean, every collector probably had started with being a RI coin

collector. So, basically it forms the base of every person's journey as a real

coin collector.

Now or

then, you would have wondered - Who proposes themes for these coins? How are

these coins released? Who decides their mintage? Who decides the denomination

and shape of coin? Can I as a numismatist suggest a theme and design of a coin?

etc... But, either non-availability of information or scattered information

left these questions unanswered.

This

article will answer all your questions regarding "Commemorative Coins of

India".

- What is a Commemorative coin?

S. 2(b) of the Coinage Act, 2011 defines "commemorative coin" as any coin stamped by the Government or any other authority empowered by the Government in this behalf to commemorate any specific occasion or event and expressed in Indian currency.

Therefore, the GoI issues commemorative coins to commemorate the birth anniversary of great leaders, or to remember any particular event with great historical significance (Dandi March-Kuka Movt etc) or others. All such issuance take place according to guidelines approved by the Govt.

During the last 1 year, the Government issued Gazette Notifications for release of 8 Commemorative Coins viz. 125th Birth Anniversary of Yogananda Paramhansa, 100 years of Jallianwala Bagh Massacre, 200th Birth Anniversary of Satguru Ram Singh ji, 550th Parkash Purab of Sri Guru Nanak Dev ji, 100th Birth Anniversary of Smt. Vijaya Raje Scindia , 100th Anniversary of Vikram Sarabhai, 150th Birth Anniversary of Mahatma Gandhi and 250th Session of Rajya Sabha. And since 2014, the Government has issued as much as 42 commemorative coins.

- Authority

The Currency and Coin Division of Department of Economic Affairs, Govt. of India is concerned with policy matters relating to production and designs of banknotes and coins, introduction of new banknotes and coins, demonetisation of any existing banknotes and coins, currency and coin related legislations, etc. Further, the matter relating to security features of Banknotes are handled by C&C Division. Security Printing and Minting Corporation of India Ltd. (SPMCIL) is under the administrative control of this Division.

The work profile of Coin section inter alia includes policy formulation regarding design, shape and size of circulation coins including fixation of fair prices of coins, coins related legislations and issuance of Commemorative Coins. Others include production planning of coins and determination of indent of coins. The production and indent of coins is strictly and regularly monitored by this section through the Meetings of Strategic Planning Committee (SPC) and Production Planning Committee (PPC).

- Guidelines

The Guidelines being followed for issue of a commemorative is not static, but a dynamic one. The revision of Guidelines was carried out on the basis of lessons learnt from the examination of proposals received by C&C Division, DEA.

The Old Guidelines for issue of commemorative coins/currency dt. 29.03.1991 was revised on 06.01.2017 by making the Guidelines more specific to coins but elaborate in nature.

The Guidelines were further revised on 25.02.2019 to incorporate a Proforma/Format for submission of proposal for commemorative coin, this was done as lots of proposals which were not as per Guidelines were received.

The most

recent revision of the Guidelines was made on 27.03.2019 to incorporate

"Commiserative Coins" viz. Commemorative Coins to be issued on

occasion to express sympathy/grief/exhibit respect for the sacrifice while

examining the proposal for issue of a commemorative coin to mark 100th

Anniversary of the Jallianwala Massacre on April 13, 2019, which was received

from the Ministry of Culture. The existing Guidelines are further re-examined

in consultation with the Ministry of Culture to make it more comprehensive.

Revised Guidelines-

The Guidelines were further revised on 25.02.2019 to incorporate a Proforma/Format for submission of proposal for commemorative coin, this was done as lots of proposals which were not as per Guidelines were received.

The most

recent revision of the Guidelines was made on 27.03.2019 to incorporate

"Commiserative Coins" viz. Commemorative Coins to be issued on

occasion to express sympathy/grief/exhibit respect for the sacrifice while

examining the proposal for issue of a commemorative coin to mark 100th

Anniversary of the Jallianwala Massacre on April 13, 2019, which was received

from the Ministry of Culture. The existing Guidelines are further re-examined

in consultation with the Ministry of Culture to make it more comprehensive.

The Central Government may issue commemorative coins of appropriate denominations by notification on eminent persons/ personalities/ institutions/ events/ programmes that have a national or international nature or have made lasting contribution or impact or reflect national/ international contribution/ impact. The contribution made by the individual organisations/ institution/ programme/ event should have transcended the barriers of partisan politics, region, community, language or religion.

However, on an occasion to express sympathy/grief/exhibit respect for the sacrifice, ‘Commiserative Coins’ would be issued.

|

| Proforma for Commemorative Coins. |

In case of subject being an Individual:

Proposal for commemorative coins shall be considered and approved subject to following guidelines:-

- The individual should be an Indian citizen or a person belonging to the Indian diaspora. The Government may commemorate an occasion related to a foreign individual, only where his or her contribution for the Indian society or humanity at large has been exceptional.

- The occasion related to the individual should be commemorated only posthumously.

- The individual should have attained excellence in public life, in areas such as science, literature, arts including performing arts of must have made intellectual contribution of an exceptional order

- The individual’s contribution should be a lasting and durable nature. A test of such durability should normally be the observance of the anniversary or birth centenary of the individual as a national occasion.

In case of subject

being an Organization/Institution/Programme/ Event

- The occasion should normally relate to a specific/ significant day of the Organization/ Institution/ Programme/ Event.

- The institution/ organization/ programme/ event should have national or international stature with significant and well recognized contribution in their field or to the Nation’s social-economic development.

- Procedure

- After examining the proposals in the light of above guidelines, a final decision in each case would be taken by the Finance Minister in consultation with the Prime Minister.

- The Government shall normally issue commemorative coins selectively and will try to issue only a minimum number of Commemorative Coins in a calendar year.

- Commemorative Coins shall conform to the dimension, designs, composition, standard weight and remedy allowed as may be specified in the notification issued by the Government prior to the release of the Commemorative Coin.

- Security Printing and Minting Corporation of India Ltd. (SPMCIL)/specified agency will mint and supply within 1 year at least 100 million pieces (mpcs) of circulation commemorative coins after release of the commemorative coin by the Govt. of India.

- Minting and distribution of Commemorative Coin will be done by SPMCIL/specified agency within a period of 1 year from the date of release

- Procedure

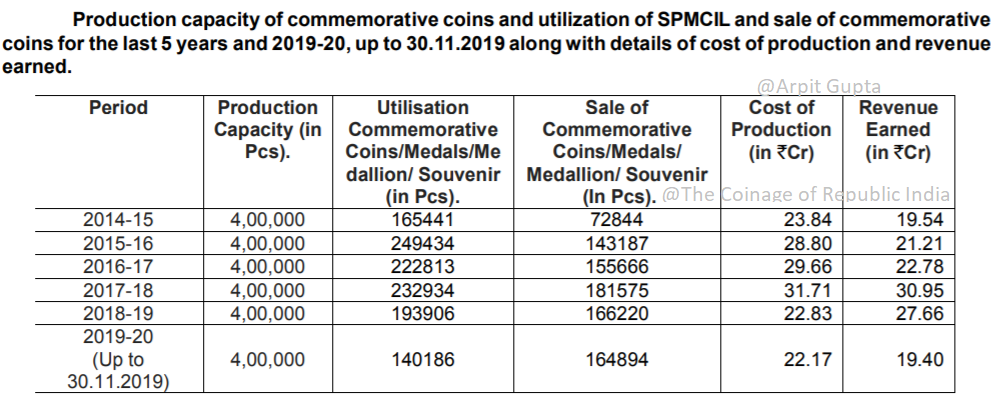

- Minting capacity

SPMCIL has a combined installed capacity of manufacturing commemorative coins in the range of 3,00,000-5,00,000 pcs per annum. Over last 5 years, on an average, SPMCIL manufactured approximately 1, 50,000 commemorative coins and medallions (per annum) for fulfilling domestic demand. This leaves sufficient spare capacity for catering to global demand.

|

| Production Capacity - Commeorative Coins |

- Pricing of Commemorative Coins

In the past, SPMCIL had been selling commemorative coins on the basis of 10% Profit Margin of the Total Cost Plus Postal Charges and Applicable GST Rate of the Total Cost. There was no policy as such for costing of commemorative coins and recovery of actual costs plus profits. To bring more clarity on the costing of commemorative coins, the Government has come out with a Policy for Costing of Commemorative Coins on 18.10.2019. This policy has been prepared in consultation with SPMCIL.

Policy for Costing:

Once the gazette notification for issuance of a commemorative coin is issued, SPMCIL starts the production of the same and also simultaneously fixes their selling price.

The sale price of a commemorative coin shall be worked out as under:

(a) General Principle: The cost incurred on minting of commemorative coins shall be recovered on cost plus principle. A profit margin shall be added depending on type of commemorative coin. The price shall be finalised before commencing the sale.

(b) Price Calculation:

(1) Metal Cost (A): Metal cost, as per metal composition and weight of each metal component in the coin is recovered as per market rates. Metal rates are based on London Metal Exchange (LME) prices or any other neutral and fair sources of Indices.

(2) Labour Cost (B): Labour cost is calculated on the basis of actual labour hours put in by workers in concerned sections of coin production by applying the actual per hour rate of labour. Design cost is also included in labour cost as per the standard costing practices.

(3) Direct Expenses/Overheads (C): Direct expenses/overheads consisting of the following are directly allocated to cost, as per the standard costing practices, being direct expense of commemorative coins: a. Die cost b. Electricity cost c. Packing Material cost There are three types of sets for packaging - Executive, Proof and UNC (Uncirculated coin). In terms of cost, Executive is at the top followed by Proof and UNC.

(4) Indirect Expenses/Overheads (D): Indirect expenses/overheads consisting of following is apportioned to cost of commemorative coins on the basis of total cost of production and units of production: a. Administration Expenses b. Security Expenses

(5) Incidental Charges (E): Incidental charges @ 20% of total cost, equalling (A+B+C+D) is also charged to cover the expenses such as marketing expenses, including advertisement expenses and sales promotion expenses, process losses, depreciation on machinery etc. Increase in any of cost components, namely Metal rates, labour charges, direct/indirect expenses is also covered through incidental charges. Further, incidental charges would also cover other costs not explicitly covered in the cost sheet e.g. capital cost, opportunity cost of own funds, process losses and contingent expenses, etc.

(6) Total Cost (F) = Metal Cost (A) + Labour cost (B) + Direct Expenses (C) + Indirect Expenses/Overheads (D) + Incidental charges (E)

(7) Profit Margin (G) = X% of Total Cost (F)

Where X=

(i) 10 for the commemorative coins minted for public personalities/events (sponsored by Ministry of Culture)

(ii) 50 for the Commemorative coins minted for public sector entities/other public autonomous bodies

(iii) 100 for private charitable sponsoring organisation

(iv) 200 for private commercial sponsoring organisation.

(8) Postal Charges (H) = Actual postal charges

(9) GST (1) = 3% of (F + G + H)

Selling Price = Total Cost (C)

+ Profit Margin (G) + Postal Charges (H) + GST (1).

(c) Minting of additional commemorative coins: Additional cost refers to the cost of production of additional lot over and above the initial planned quantity. There may not be any additional cost for minting of second and subsequent lots of commemorative coins and these coins are minted at essentially the same cost. However, to absorb the ramp up costs, and some other incidentals as well as to encourage single-go orders, each additional coin will be billed at 1.10 times the cost of initial lot.

I hope this article helps answering most of the common queries, feel free to share your views!

References:

- Department of Economic Affairs (DEA), GoI

- The Coinage Act, 2011

- The Coinage of Republic India by Arpit Gupta

|

Selling Price = Total Cost (C)

+ Profit Margin (G) + Postal Charges (H) + GST (1).

|

I hope this article helps answering most of the common queries, feel free to share your views!